e-Way Bill is an electronic way bill for the movement of goods to be generated on the e-way bill portal. e-Way Bill is required for a transparent and hassle-free movement of goods across India.

Latest Update

29th August 2021 From 1st May 2021 to 18th August 2021, the taxpayers will not face blocking of e-way bills for non-filing of GSTR-1 or GSTR-3B (two months or more for monthly filer and one quarter or more for QRMP taxpayers) for March 2021 to May 2021.

4th August 2021 Blocking of e-way bills due to non-filing of GSTR-3B resumes from 15th August 2021.

1st June 2021 1. The e-way bill portal, in its release notes, has clarified that a suspended GSTIN cannot generate an e-way bill. However, a suspended GSTIN as a recipient or as a transporter can get a generated e-way bill. 2. the mode of transport 'Ship' has now been updated to 'Ship/Road cum Ship' so that the user can enter a vehicle number where goods are initially moved by road and a bill of lading number and date for movement by ship. This will help in availing the ODC benefits for movement using ships and facilitate the updating of vehicle details as and when moved on road.

18th May 2021 The CBIC in Notification 15/2021-Central Tax has notified that the blocking of GSTINs for e-Way Bill generation is now considered only for the defaulting supplier's GSTIN and not for the defaulting recipient or the transporter's GSTIN.

An overview of e-Way Bills in Form EWB-01

Form GST EWB-01 is the e-way billdocument that needs to be carried by the person in charge of the conveyance for movement of goods where the value of the consignment exceeds Rs. 50,000 whether or not a supply. The e-way bill format contains the details of the sender, receiver and the transporter (if the seller is not the transporter).

Value of consignment means the value of goods mentioned in the invoice/ bill of supply/ challan and shall include the taxes in the form of CGST/ SGST/ IGST. However, the value of goods excludes the value of any exempt goods billed together with taxable goods.

The consignor or consignee should generate the e-way bill when the value of goods transported is more than Rs. 50,000 (each consignment or all consignments put together) in their own vehicle/railways/ airways/ ship. However, where transport is by road, and the consignor/consignee does not generate the e-way bill as the case may be, the onus lies on the transporter/GTA to generate the e-way bill. The transporter/GTA has to generate an e-way bill based on the consignor's Part-A/ invoice details.

Mandatory cases in which an EWB-01 is to be generated

e-Way Bill has to be generated even if the value of goods is below Rs. 50,000 for the following:

1. Job-Work: Goods sent by the principal from one state to a job worker in another state.

2. Handicraft Goods: e-way bill should also be generated in the inter-state transport of goods by a dealer exempt from GST Registration.

Modes available to generate e-way bills

A user has to register on the common portal of e-way bills before starting using the services. e-Way Bills can be generated in a number of ways. GSTN has provided the following modes for generating e-way bills:

Online: Anyone can log in to the e-way bill portal as the user or sub-user as the case may be. Then click on the 'Generate new' option under the main tab 'e-way bill' appearing on the left-hand side of the dashboard.

Via SMS: A very convenient on-the-go option for generating e-way bills has been introduced under GST. One can use this mode at times of emergency.

Use Bulk-generation offline tool: To generate multiple e-way bills by a single upload of JSON file. This facility may be used by businesses having a large number of consignments to be delivered.

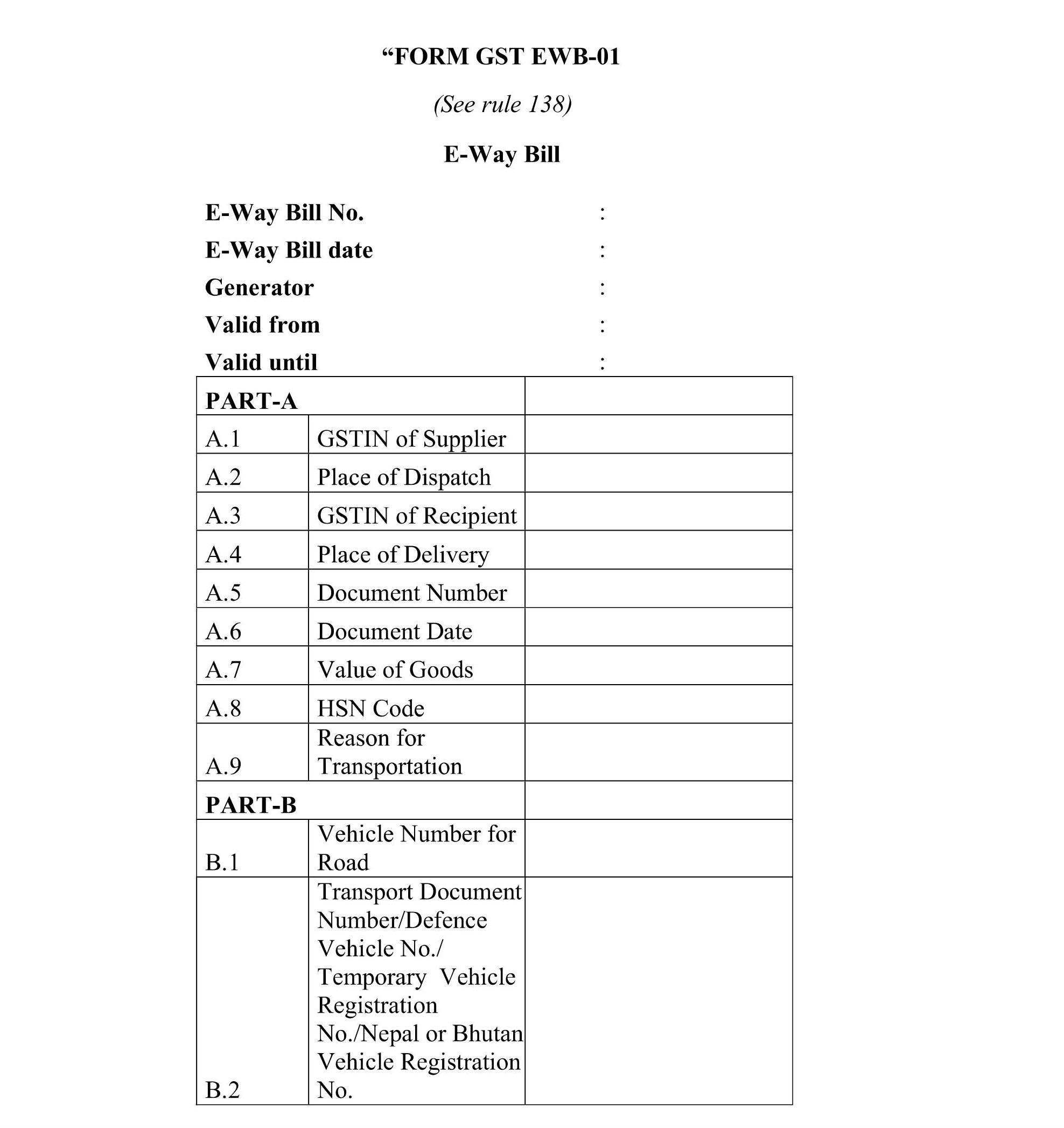

Format of Form GST EWB-01 explained

The EWB-01 has to be generated online on the e-way bill portal. The form GST EWB-01 consists of the 12-digit e-way bill number, date of the generation with the name of generator, validity period of the e-way bill. The contents of the form can be divided into two parts as follows:

PART A

PART B

GSTIN of Supplier and/or Recipient

Place of Dispatch-PIN Code of Place

Place of Delivery – PIN Code of Place

Invoice/Challan Number, Date and Value of Goods

HSN Code – At least 2 digits of the HSN Code

Reason for Transport – Supply, Export, Import, Job Work, sales return, exhibition, For Own use etc.

Transporter Doc. No./ Defence Vehicle No./ Temporary Vehicle Registration No./ Nepal or Bhutan Vehicle Registration No. – Document Number provided by the transporter

Vehicle Number in which goods are transported

The view of the form as laid down in the rules is as follows:

Part-A has to be filled at the time of generation of the e-way bill by:

The supplier or

The recipient where the supplier is unregistered or

The e-commerce operator, if supplied on an e-commerce platform

The transporter, if no e-Way Bill was generated for that invoice/challan by supplier/ recipient as the case may be

Part-B with vehicle or conveyance details must be filled up if the supplier himself is transporting goods on either own or hired a conveyance. However, the supplier can send details of Part-A of the e-way bill to the transporter when using the transporter services. Then the transporter generates an e-way bill filling up Part-B and only after being authorised by that supplier.

However, Part-B details are not required where the goods are transported for a distance of less than fifty* kilometres within the State or Union territory between consignor-consignee place.

*changed with effect from 7th March 2018

The view of the form as laid down in the rules is as follows:

The view of how the e-Way Bill looks like when generated online

Note the QR code at the top of the e-way bill that can be scanned with the reader to get more consignment details or the generator. In addition, the person-in-charge of the vehicle can now carry a copy of the e-way bill or the EWB number in the following ways:

Physically

Mapped to a Radio Frequency Identification Device (RFID) embedded on to the conveyance after being permitted by the Commissioner

How to download and save an e-way bill in pdf format

You can download the save the e-way bill by following the below steps

Step 1: Log in to the e-way bill portal and click on 'Print EWB' under the 'e-way bill' tab.

Step 2: Enter the e-way bill number and click on 'GO'.

Step 3: The e-way bill details will be displayed and then click on the 'Print' button available below.

Step 4: Select the destination as 'Microsoft Print to PDF' or 'Save as PDF' and select the desired location where you want to save the e-way bill.

Note: You can print or download the detailed e-way bill by clicking on 'Detailed Print'.

Frequently Asked Questions

How e-way bill needs to be generated in case of supply of goods by an unregistered person to a registered person?

Where the supply of goods is made by an unregistered person to a registered person, the e-way bill shall be generated by the recipient of such goods, as for the purpose of supply he is said to be the person causing the movement of goods. Therefore, the recipient, in this case, would generate an e-way bill by furnishing details in Part-A of FORM GST EWB – 01

Whether an e-way bill will be required if transportation is done in one's own vehicle or through public transport?

Yes, an e-Way bill is required to be generated where the consignor or consignee transports the goods in his own vehicle or a hired one. In such a case, the person causing the movement of goods may raise the e-way bill after furnishing the vehicle no. in Part-B of Form GST EWB – 01 if the value is more than Rs.50,000/-.

Under this circumstance, the person can himself generate the e-way bill if registered in the portal as the taxpayer. If the person is unregistered or an end consumer, they need to get the e-way bill generated from the taxpayer or supplier based on the bill or invoice. Alternatively, he can enrol and log in as a citizen and generate the e-way bill.

Whether the validity of e-way bills starts from updating Vehicle number or even an update of Transporter ID?

The e-way bill is generated when the details related to the vehicle number are furnished in Part-B of Form GST EWB-01. Therefore, the validity of the e-way bill will start from the date when the vehicle number will be updated in such form, not merely on updating the transporter ID.

What if the vehicle is stuck at a particular point in the journey due to calamity or traffic jam?

The goods are required to be transported within the validity period of the e-way bill. However, it is provided that under circumstances of exceptional nature, the transporter may generate another e-way bill after updating the details in Part-B of Form GST EWB-01. These circumstances could be said to be exceptional. However, further clarification is required in the absence of a specific meaning of the term "exceptional nature".

What happens when there is a change of transporter? Say transporter A generates an e-way bill and hands over goods to transporter B after some movement?

The consignor, consignee or transporter may assign the e-way bill number to another registered or enrolled transporter for updating the information in Part-B of Form GST EWB-01 for further movement of consignment. But once the details have been uploaded in Part-B by the transporter, such e-way bill numbers shall not be allowed to be assigned to any other transporter. Hence, any changes in Part-B of the e-way bill may be made only by transporter "A", not by transporter "B".

What is the transport document number mentioned under Part-A of EWB -01?

The government amended GST rules on 23rd January 2018 to include the transport document number to the Part-B of Form GST EWB-01. The transport document number indicates the goods receipt number or railway receipt number or airway bill number or bill of lading number issued by the respective transporter, as may be selected by the person.

India's Fastest and Most Advanced 2B Matching

Maximise ITC claims, use smart validations to correct your data and complete 2B matching in <1 minute

Post a Comment for "E Way Bill Format Pdf Download"